Business Combinations and consequent Purchase Price Allocation

This article discusses matters related to inter-alia principles on Business Combinations, Purchase Price Allocation and Integral Valuation analysis

5/13/20247 min read

Meaning

Ind AS 103 / IFRS 3 on Business Combinations, defines Business Combinations as a transaction or other event in which an acquirer obtains control of one or more businesses.

As per US GAAP ASC 805, a Business Combination is a transaction in which an acquirer obtains control over one or more businesses.

Accounting – Recognition and Measurement

As per Ind AS 103 / IFRS 3, Business combinations are accounted for using the acquisition method which requires following:

identifying the acquirer (the acquirer is the entity that obtains control of another entity);

determining the acquisition date (the date on which the acquirer obtains control);

recognise and measure the identifiable assets acquired and the liabilities assumed and non-controlling interest; and

recognise and measure any goodwill or bargain purchase.

As of the acquisition date, the acquirer shall recognize, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree.

The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date fair values.

Need for Purchase Price Allocation (‘PPA’) analysis

Various GAAPs (USGAAP, IFRS, Ind AS) require that the fair value of assets and liabilities acquired in a business combination be recognized in the financial statements of the acquirer entity. PPA is the process whereby allocation of purchase price / consideration paid for an acquired business among the identifiable assets (including intangible assets) and liabilities assumed is made. PPA is required to ensure that the financial statements of the acquirer entity reflect the fair value of the assets and liabilities acquired in the business combination. This provides more accurate picture of the financial performance and position of the acquirer entity after business combination transaction. PPA also helps to calculate the amount of goodwill recognized pursuant to business combination transaction. Goodwill represents the excess of the purchase price over the fair value of the identifiable assets and liabilities acquired. The amount of goodwill recognized in the business combination can have significant implications for financial reporting, taxation and future impairment testing.

A fairly complex process, it requires in-depth domain knowledge, understanding of the business plan, and expertise in intrinsic valuation to ensure all aspects of the analysis have been factored in correctly. From valuation point of view, intangible assets valuation is most complex and important in PPA exercise.

Few critical parameters that need to be analyzed before initiating valuation of intangible assets for the purpose of PPA

Business Entity Valuation

Business valuation is important when valuing intangible assets to ensure that the prospective financial information used in the valuation is market participant specific and does not include any acquirer specific synergy.

Market participant specific refers to the perspective of a hypothetical buyer and seller in the market for the intangible asset, who are assumed to be independent and well-informed. In other words, the valuation should reflect the value that would be assigned to the intangible asset by a third-party buyer who is not a strategic buyer or acquirer with a specific reason for acquiring the asset, such as cost savings or synergy. Including acquirer-specific synergies in the valuation can result in an inflated value that does not reflect the market value of the intangible asset. This is because the synergies may not be replicable by other market participants and may not reflect the true value of the intangible asset on a standalone basis.

To ensure this, we need to compute Internal rate of Return ('IRR') which here represents implied return from the transaction using prospective financial information of the acquired business that may include acquirer-specific elements.

Weighted Average Cost of Capital ('WACC') represents the average expected return from the business for a market participant investor and includes an element to compensate for the average risk associated with potential realization of these cash flows.

If WACC and IRR are literally same, it can be concluded that prospective financial information is market participant expected cash flows and the consideration transferred equals the fair value of the business acquired.

In simple words, to ensure that prospective financial information is market participant specific and does not include any acquirer specific synergy benefits, we should carry out the business valuation of the Company (acquired business) and arrive at the implied discount rate at which the Equity value equals the fair value of the Purchase Consideration. The implied discount rate / IRR so arrived is then compared with the Industry WACC.

Measurement of consideration transferred including contingent consideration

Contingent consideration is a financial arrangement in which an acquirer agrees to make additional payments to the seller of a business if certain performance criteria are met in the future. The measurement of contingent consideration depends on the specific terms of the agreement.

In general, contingent consideration should be measured at fair value at the acquisition date. The fair value of contingent consideration should be estimated using a probability-weighted approach that considers the likelihood of achieving the performance criteria and the amount of the potential payments.

To determine the fair value of contingent consideration, companies may use various techniques, such as discounted cash flow analysis, option pricing models, or Monte Carlo simulations. The assumptions and inputs used in these models should be based on reasonable and supportable information, including market data, historical performance, and management's expectations.

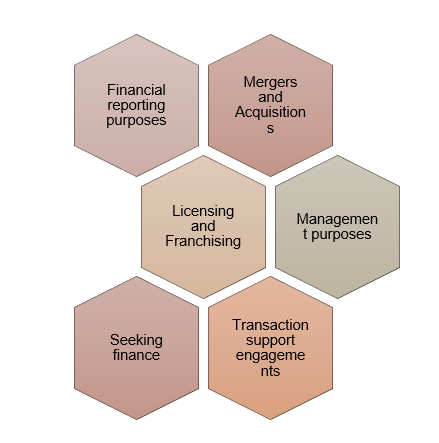

Purposes of Intangible Asset valuations

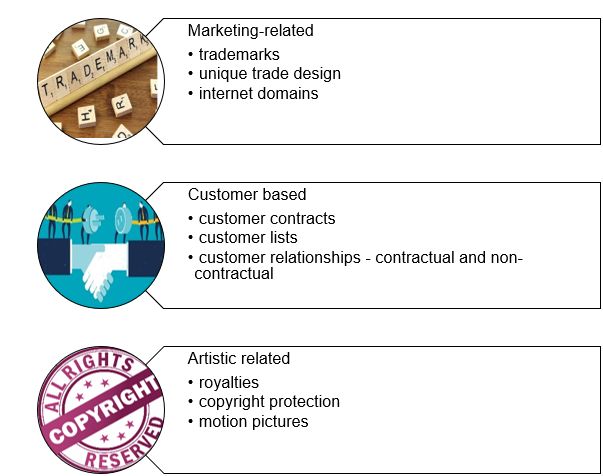

Broad categories of Intangible assets with few examples

Valuation Aspects

Out of the three approaches viz. Cost, Market and Income for valuation of Intangible Assets, Income approach is the most common applied method and is frequently used to value intangible assets mentioned above.

Following are the popular methods under Income Approach -

excess earnings method i.e., Multi-Period Excess Earning Method (‘MEEM’)

with and without method

relief from royalty method

greenfield method and

distributor method

In this edition, we are focusing on the first method i.e., excess earnings method.

Let us consider valuing customer relationship based intangible asset by using multi-period excess earnings method -

Valuation of customer relationship based intangible asset

i) Meaning

Customer-related intangible assets include customer lists, backlog, customer contracts and contractual and non-contractual customer relationships.

A valuation analyst should consider important elements that create this intangible asset which are mentioned below –

For customer relationship based intangible asset to exist, it must have informational component or factual information about the customer like name, contact details, buying preferences etc. which can be useful to the Company.

There is an expectation form such customer relationship for recurring business for the Company.

Customer-related intangible assets create value for a definite finite period. Over period of time, customer lists will reduce due to customer mortality, competition etc.

These assets often create value for the company along with use of other assets by the company to generate earnings e.g., property, plant and equipment, working capital, other intangible assets etc.

ii) Important steps for valuation of customer relationship based intangible asset under MEEM

Revenue estimate with appropriate attrition

Contributory Asset charge

Rate of return / Risk-adjusted discount rate

Economic life

Tax Amortization benefit

Let us understand now each step in detail -

a) Revenue and cash flow estimate with appropriate attrition

Under this method, revenue and cash flows derived from the subject intangible asset needs to be determined and then cash flows attributed to Contributory assets needs to be deducted. This requires estimating the revenue from repeat business from existing customers as of the valuation date. Since the customer relationship assets derive value for a finite period, the number of customers providing business in future reduces over period of time. Attrition is the measurement of loss of existing customers. Here, if historical data is available, it may be used to arrive at the expected annual attrition rate. The attrition rate so arrived is then applied to projected revenue stream from existing customers to arrive at the expected revenue over the period of economic life of this asset.

b) Contributory Asset Charges (‘CACs’)

There are various other assets in the category of property, plant and equipment, working capital, other intangible assets etc. which contributes in generating the projected revenue from the use of the existing customer relationships. Since the earnings from customer-relationship based intangible asset depends on these assets, the valuer must estimate the CACs to exclude the incremental cash flows attributable to customer relationship based intangible asset. Any non-operating assets which don’t contribute in the estimated earnings should note be considered as contributory assets. The amount that should be deducted is typically the alternative costs for the contributory assets or the income such assets would generate in a different use if they were not used in connection with the subject intangible asset.

c) Rate of return / Risk-adjusted discount rate

The determination of the appropriate discount rate to be used to estimate an intangible asset’s fair value requires additional consideration as compared to those used when selecting a discount rate to determine enterprise value.

Selecting discount rates for intangible assets can be challenging as observable market evidence of discount rates for intangible assets is rare. The selection of a discount rate for an intangible asset generally requires significant professional judgment. In selecting a discount rate for an intangible asset, valuers should perform an assessment of the risks associated with the subject intangible asset and consider observable discount rate benchmarks.

When assessing the risks associated with an intangible asset, a valuer should consider factors including the following:

intangible assets often have higher risk than tangible assets,

if an intangible asset is highly specialized to its current use it may have higher risk than assets with other potential uses,

single intangible assets may have more risk than groups of assets (or businesses),

intangible assets used in risky (sometimes referred to as non-routine) functions may have higher risk than intangible assets used in more low-risk or routine activities.

the life of the asset. Similar to other investments, intangible assets with longer lives are often considered to have higher risk,

intangible assets with more readily estimable cash flow streams, such as backlog, may have lower risk than similar intangible assets with less estimable cash flows such as customer relationships.

d) Economic life

An important consideration in the valuation of an intangible asset is the economic life of the asset. This may be a finite period limited by legal, technological, functional or economic factors; other assets may have an indefinite life.

For customer related intangibles, attrition is a key factor in estimating an economic life as well as the cash flows used to value the customer related intangibles. Attrition applied in the valuation of intangible assets is a quantification of expectations regarding future losses of customers. While it is a forward-looking estimate, attrition is often based on historical observations of attrition.

e) Tax Amortization Benefit (‘TAB’)

The effect of income taxes should be considered when an intangible asset’s fair value is estimated as part of a business combination, an asset acquisition, or an impairment analysis.

The present value of the intangible asset’s projected cash flows should reflect the tax saving that may result from claiming of depreciation on such intangible asset. If the market or cost approach is used to value an intangible asset, the price paid to create or purchase the asset would already reflect the ability to amortize the asset. However, in the income approach, a TAB needs to be explicitly calculated and added

Meaning

Ind AS 103 / IFRS 3 on Business Combinations, defines Business Combinations as a transaction or other event in which an acquirer obtains control of one or more businesses.

As per US GAAP ASC 805, a Business Combination is a transaction in which an acquirer obtains control over one or more businesses.

Accounting – Recognition and Measurement

As per Ind AS 103 / IFRS 3, Business combinations are accounted for using the acquisition method which requires following:

identifying the acquirer (the acquirer is the entity that obtains control of another entity);

determining the acquisition date (the date on which the acquirer obtains control);

recognise and measure the identifiable assets acquired and the liabilities assumed and non-controlling interest; and

recognise and measure any goodwill or bargain purchase.

As of the acquisition date, the acquirer shall recognize, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree.

The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date fair values.

Need for Purchase Price Allocation (‘PPA’) analysis

Various GAAPs (USGAAP, IFRS, Ind AS) require that the fair value of assets and liabilities acquired in a business combination be recognized in the financial statements of the acquirer entity. PPA is the process whereby allocation of purchase price / consideration paid for an acquired business among the identifiable assets (including intangible assets) and liabilities assumed is made. PPA is required to ensure that the financial statements of the acquirer entity reflect the fair value of the assets and liabilities acquired in the business combination. This provides more accurate picture of the financial performance and position of the acquirer entity after business combination transaction. PPA also helps to calculate the amount of goodwill recognized pursuant to business combination transaction. Goodwill represents the excess of the purchase price over the fair value of the identifiable assets and liabilities acquired. The amount of goodwill recognized in the business combination can have significant implications for financial reporting, taxation and future impairment testing.

A fairly complex process, it requires in-depth domain knowledge, understanding of the business plan, and expertise in intrinsic valuation to ensure all aspects of the analysis have been factored in correctly. From valuation point of view, intangible assets valuation is most complex and important in PPA exercise.

Few critical parameters that need to be analyzed before initiating valuation of intangible assets for the purpose of PPA

Business Entity Valuation

Business valuation is important when valuing intangible assets to ensure that the prospective financial information used in the valuation is market participant specific and does not include any acquirer specific synergy.

Market participant specific refers to the perspective of a hypothetical buyer and seller in the market for the intangible asset, who are assumed to be independent and well-informed. In other words, the valuation should reflect the value that would be assigned to the intangible asset by a third-party buyer who is not a strategic buyer or acquirer with a specific reason for acquiring the asset, such as cost savings or synergy. Including acquirer-specific synergies in the valuation can result in an inflated value that does not reflect the market value of the intangible asset. This is because the synergies may not be replicable by other market participants and may not reflect the true value of the intangible asset on a standalone basis.

To ensure this, we need to compute Internal rate of Return ('IRR') which here represents implied return from the transaction using prospective financial information of the acquired business that may include acquirer-specific elements.

Weighted Average Cost of Capital ('WACC') represents the average expected return from the business for a market participant investor and includes an element to compensate for the average risk associated with potential realization of these cash flows.

If WACC and IRR are literally same, it can be concluded that prospective financial information is market participant expected cash flows and the consideration transferred equals the fair value of the business acquired.

In simple words, to ensure that prospective financial information is market participant specific and does not include any acquirer specific synergy benefits, we should carry out the business valuation of the Company (acquired business) and arrive at the implied discount rate at which the Equity value equals the fair value of the Purchase Consideration. The implied discount rate / IRR so arrived is then compared with the Industry WACC.

Measurement of consideration transferred including contingent consideration

Contingent consideration is a financial arrangement in which an acquirer agrees to make additional payments to the seller of a business if certain performance criteria are met in the future. The measurement of contingent consideration depends on the specific terms of the agreement.

In general, contingent consideration should be measured at fair value at the acquisition date. The fair value of contingent consideration should be estimated using a probability-weighted approach that considers the likelihood of achieving the performance criteria and the amount of the potential payments.

To determine the fair value of contingent consideration, companies may use various techniques, such as discounted cash flow analysis, option pricing models, or Monte Carlo simulations. The assumptions and inputs used in these models should be based on reasonable and supportable information, including market data, historical performance, and management's expectations.

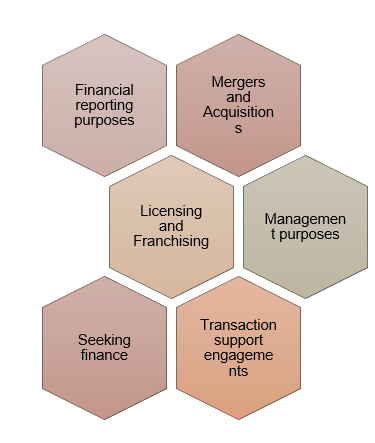

Purposes of Intangible Asset valuations

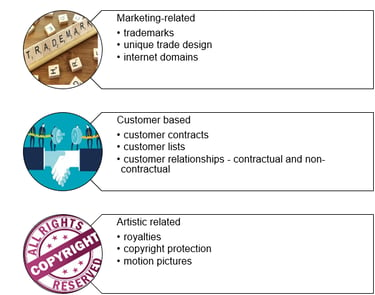

Broad categories of Intangible assets with few examples

Valuation Aspects

Out of the three approaches viz. Cost, Market and Income for valuation of Intangible Assets, Income approach is the most common applied method and is frequently used to value intangible assets mentioned above.

Following are the popular methods under Income Approach -

excess earnings method i.e., Multi-Period Excess Earning Method (‘MEEM’)

with and without method

relief from royalty method

greenfield method and

distributor method

In this edition, we are focusing on the first method i.e., excess earnings method.

Let us consider valuing customer relationship based intangible asset by using multi-period excess earnings method -

Valuation of customer relationship based intangible asset

i) Meaning

Customer-related intangible assets include customer lists, backlog, customer contracts and contractual and non-contractual customer relationships.

A valuation analyst should consider important elements that create this intangible asset which are mentioned below –

For customer relationship based intangible asset to exist, it must have informational component or factual information about the customer like name, contact details, buying preferences etc. which can be useful to the Company.

There is an expectation form such customer relationship for recurring business for the Company.

Customer-related intangible assets create value for a definite finite period. Over period of time, customer lists will reduce due to customer mortality, competition etc.

These assets often create value for the company along with use of other assets by the company to generate earnings e.g., property, plant and equipment, working capital, other intangible assets etc.

ii) Important steps for valuation of customer relationship based intangible asset under MEEM

Revenue estimate with appropriate attrition

Contributory Asset charge

Rate of return / Risk-adjusted discount rate

Economic life

Tax Amortization benefit

Let us understand now each step in detail -

a) Revenue and cash flow estimate with appropriate attrition

Under this method, revenue and cash flows derived from the subject intangible asset needs to be determined and then cash flows attributed to Contributory assets needs to be deducted. This requires estimating the revenue from repeat business from existing customers as of the valuation date. Since the customer relationship assets derive value for a finite period, the number of customers providing business in future reduces over period of time. Attrition is the measurement of loss of existing customers. Here, if historical data is available, it may be used to arrive at the expected annual attrition rate. The attrition rate so arrived is then applied to projected revenue stream from existing customers to arrive at the expected revenue over the period of economic life of this asset.

b) Contributory Asset Charges (‘CACs’)

There are various other assets in the category of property, plant and equipment, working capital, other intangible assets etc. which contributes in generating the projected revenue from the use of the existing customer relationships. Since the earnings from customer-relationship based intangible asset depends on these assets, the valuer must estimate the CACs to exclude the incremental cash flows attributable to customer relationship based intangible asset. Any non-operating assets which don’t contribute in the estimated earnings should note be considered as contributory assets. The amount that should be deducted is typically the alternative costs for the contributory assets or the income such assets would generate in a different use if they were not used in connection with the subject intangible asset.

c) Rate of return / Risk-adjusted discount rate

The determination of the appropriate discount rate to be used to estimate an intangible asset’s fair value requires additional consideration as compared to those used when selecting a discount rate to determine enterprise value.

Selecting discount rates for intangible assets can be challenging as observable market evidence of discount rates for intangible assets is rare. The selection of a discount rate for an intangible asset generally requires significant professional judgment. In selecting a discount rate for an intangible asset, valuers should perform an assessment of the risks associated with the subject intangible asset and consider observable discount rate benchmarks.

When assessing the risks associated with an intangible asset, a valuer should consider factors including the following:

intangible assets often have higher risk than tangible assets,

if an intangible asset is highly specialized to its current use it may have higher risk than assets with other potential uses,

single intangible assets may have more risk than groups of assets (or businesses),

intangible assets used in risky (sometimes referred to as non-routine) functions may have higher risk than intangible assets used in more low-risk or routine activities.

the life of the asset. Similar to other investments, intangible assets with longer lives are often considered to have higher risk,

intangible assets with more readily estimable cash flow streams, such as backlog, may have lower risk than similar intangible assets with less estimable cash flows such as customer relationships.

d) Economic life

An important consideration in the valuation of an intangible asset is the economic life of the asset. This may be a finite period limited by legal, technological, functional or economic factors; other assets may have an indefinite life.

For customer related intangibles, attrition is a key factor in estimating an economic life as well as the cash flows used to value the customer related intangibles. Attrition applied in the valuation of intangible assets is a quantification of expectations regarding future losses of customers. While it is a forward-looking estimate, attrition is often based on historical observations of attrition.

e) Tax Amortization Benefit (‘TAB’)

The effect of income taxes should be considered when an intangible asset’s fair value is estimated as part of a business combination, an asset acquisition, or an impairment analysis.

The present value of the intangible asset’s projected cash flows should reflect the tax saving that may result from claiming of depreciation on such intangible asset. If the market or cost approach is used to value an intangible asset, the price paid to create or purchase the asset would already reflect the ability to amortize the asset. However, in the income approach, a TAB needs to be explicitly calculated and added