Decoding critical aspects of Start-Up Companies

This article discusses matters related to inter-alia present start-up ecosystem, Budget 2023 announcements specific to start-ups, important factors affecting its valuation and and various valuation methodologies

5/13/20248 min read

Meaning

In simple terms, start-ups are companies incorporated with sole objective of solving critical mass level problems by developing a unique product or service. In a way start-ups tend to remedy deficiencies of existing products and services or may also create altogether new categories of goods and services thereby disrupting generic ways of thinking and doing business for various industries. Hence, we often find a word “Disruption” for any talks hovering around start-ups. Use of technology is almost an integral part of any start-up.

Start-up landscape in India

Start-ups were in existence since 1990s but only in 2010s that many of today’s best-known start-ups stepped into the limelight. Indian startup ecosystem finally got big policy push from the Indian Government in the name of Start-up India to take India’s tech economy to the next level on January 16, 2016, which is why the day is celebrated as National Startup Day since then every year. This launch gave the most needed boost and have helped India widen its footprints in the global start-up ecosystem. Seven years since then been about the journey of the Indian start-up ecosystem and like a start-up – 2016 was the beginning, followed by unabated growth, the speed bumps of 2022 and now hope of maturity and sustainability in 2023.

Today, the country has the third largest start-up ecosystem anywhere in the world, according to the Ministry of Commerce and Industry (‘MoCI’). India has around 108 unicorns with a total valuation of around $350 billion of which 21 unicorns with a valuation of $26.99 billion were born in 2022. Approx. 84000 start-ups being recognized in the Country till 2022 (MoCI).

In a recent address at the 108th India Science Congress (ISC), honorable Prime Minister Shri Narendra Modiji stated that with regards to innovation in start-ups, India ranks among the world’s top three countries. He also referred findings of the Global Innovation Index 2022, released by the World Intellectual Property Organisation (WIPO) in September 2022, which placed India at the 40th position among 132 countries.

Sustained government efforts through several programs under the Start-up India Initiative, have not only resulted in the rise of the number of start-ups but also created lakhs of jobs in the Country. To further boost growth, the government has affected slew of measures outlook to bring reforms in the start-up ecosystem. These can be summarized as below:

Financial support

Support private investment in start-ups using AIFs and incubators

Start-up India Seed Fund Scheme (‘SISFS’)

Credit Guarantee Scheme for Start-ups (‘CGSS’) for credit provided by banks and other financial institutions to DPIIT-recognized start-ups

Most recently in 2022, the government announced the rollout of the Digital India Start-up Hub and launched the SETU - Supporting Entrepreneurs in Transformation and Upskilling programme to connect start-ups in India to US-based investors and start-up ecosystem leaders, among others. These are besides other measures like the Fund of Funds for Start-ups (‘FFS’) Scheme, Support for Intellectual Property Protection (‘SIPP’), Income Tax exemption for three years, and National Start-up Awards (NSA) which all supplement start-up growth in the country.

What is there in Budget 2023 for Start-ups

FM Sitharaman has announced a slew of measures to further boost start-ups in India. These are summarized as below:

Relief to start-ups in carrying forward and setting off of losses from existing 7 years to 10 years.

Eligible start-ups incorporated between April 1, 2016 to April 1, 2023 were eligible for tax holiday under section 80 – IAC. The period of incorporation proposed to be extended by one year to April 1, 2024.

Further, the government had allocated Rs 283.5 crore for the SISFS, which was higher than the Revised Estimates of about Rs 100 crore in the previous budget. The budgetary allocations for the FFS stood at Rs 1,000 crore.

Further, to unleash innovation and research by start-ups, a National Data Governance Policy will be brought out. This will enable access to anonymized data. Further, an Agriculture Accelerator Fund will be set-up to encourage agristart-ups by young entrepreneurs in rural areas. The Fund will aim at bringing innovative and affordable solutions for challenges faced by farmers.

The budget measure comes when the start-up sector is seeing a funding winter as investors only put in approximately $25 billion in Indian start-ups in 2022, a 40 percent drop from the $42 billion raised across 1,500+ deals in 2021.

Further, Section 56(2)(viib) has been proposed to be amended w.e.f. AY2024-25 to extend its applicability to tax share premium received from NR investors (presently applicable to resident investors only) in a closely held company in excess of its fair market value.

Important factors affecting valuation of start-ups especially an early stage / pre-revenue start-ups

It is indeed more difficult to value an early-stage start-up company without any actual revenue. Fundamentally, it is too different to value a start-up than valuing an existing company. Reliance on mere financial projections and quantitative analysis is not useful and emphasize must be given on other qualitative parameters.

For most of early-stage companies, there is no sound finance system. For the investors focusing on start-ups, one of the most difficult tasks is determining how to price the investment. In other words, the investors need to decide on the amount of equity or ownership interest they should get in exchange for the invested capital, whereas the entrepreneurs are concerned about the amount of equity they will need to issue. Deciding on the amount of ownership interest requires determining the enterprise value (EV) / equity value.

Major factors that should be considered while valuing these start-ups can be summarized as under:

Traction

Traction refers to the progress that company has made, or the momentum company has attained over a while, keeping in mind its potential customers. Having reasonable traction reduces uncertainty in terms of implementation from business idea. Accordingly, traction metrics which are quantifiable helps investors in decision-making.

This can be assessed basis following parameters: -

Userbase

Existing customer base is most important. The greater the number, the better.

Marketing effectiveness

If you can demonstrate that you can acquire customers with low acquisition cost which is commonly described as Customer acquisition cost (CAC), this will draw interest of pre-revenue investors.

Growth rate

Representing that your business has grown with limited funds helps getting investors’ confidence.

Serial / experienced start-up founders never skip to put traction metrics in their pitch-deck / presentation like EBITDA margin, CAC, MoM revenue growth, Product development (new features, technology) etc.

Founders’ Team

Especially for pre-revenue / early-stage start-ups, founders’ team is one of the most important factor to consider before making an investment. Founders with proven experience, diversified skills and competence and 100% commitment towards the start-up (i.e., no side businesses) is of much significance.

Minimum Viable Product (‘MVP’)

This enables start-up to showcase features and benefits of the product or service to prospective investors. This in reality demonstrates vision of founders for turning ideas into reality.

Market

If the start-up is in such industry which is unique as well as booming, it will attract more investors against the space where multiple founders are working upon.

High margins

Businesses with high operating and net margin coupled with high growth on revenue side are more appealing to investors than other ones.

Start-up Valuations

Business valuation is an important facet, need for which arises in case of fund raise, mergers, acquisitions, issuance of employee stock options, financial reporting purpose etc. Unlike established businesses which generally have detailed projected financial statements in line with historic trend in terms of revenue and margins, set of customers, clearly defined revenue streams, assets and other factors, early stage start-ups lacks in all these which makes it more difficult to value the business of the start-ups. Also, start-ups valuation changes very often due to exponential growth especially in early phase.

Following are some common methods for start-up valuations at early / pre-revenue stage

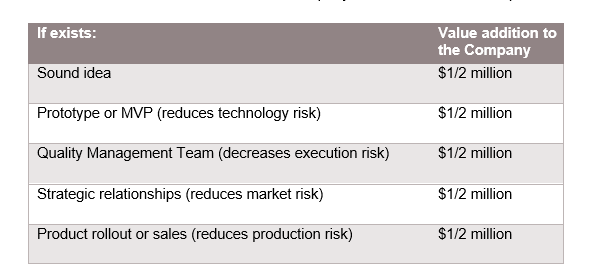

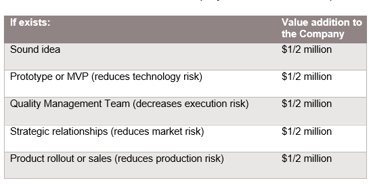

i. The Berkus Method

Very few start-ups in reality meet or exceed the projected revenues in the explicit forecast period. Accordingly, one of the reasonable and best method to value pre-revenue start-ups is to value a start-up to give the value to those elements of progress by the entrepreneur or team that reduces risk of success. This method assigns a number, a financial valuation to each of the four major elements of risk faced by pre-revenue and early stage companies. For each element, the method adds maximum of half a USD million in value to arrive at overall company’s valuation. This can be presented in the below table:

If exists:

Value ad

Maximum value of Company under this method can be $ 2.5 million.

ii. Scorecard valuation method

This method is based on the comparison. This is widely used method among angel investors. In this method, the target start-up seeking investment is compared with other similar funded start-ups. The scorecard method is used to compare the target company to another similar companies in the industry/average of group of such start-ups. The basis on which they compare the companies are the stage of development, business sector, and geographic location. Before adjusting the median of the appraisal, the target company will be compared with others by the investor for several factors. This will value the company level and help them decide the amount they would invest in the company. The scorecard valuation model helps determine the average value of the target company. The scorecard method is the most popular way to derive a pre-money value.

The main criteria for the scorecard method in order are:

Board, entrepreneur, the management team – 25%

Size of opportunity – 20%

Technology/Product – 18%

Marketing/Sales – 15%

Need for additional financing – 10%

Others – 10%

Accordingly, once you determine the pre-money average valuation of comparable businesses, you need to compare your company to the traits listed above. After that, assign a comparison % to each quality. When compared to your competition, you can be at par, below average or above average for each of the listed characteristic.

iii. Risk Summation Method

This method has a bit more quantitative workings on specific risk factors, which brings further risk management and governance consideration into the pre-money valuation. This can be used together with Scorecard method. Following risks associated with the start-up and its industry are addressed:

Management risk

Stage of the business

Legislation/Political risk

Manufacturing risk (or supply chain risk)

Sales and marketing risk

Funding/capital raising risk

Competition risk

Technology risk

Litigation risk

International risk

Reputation risk

Exit value risk

Instead of assigning percentage weights and multiples, assignment of the ratings (+2 to -2) to each risk factor and do an adjustment to the average pre-money valuation per each rating. For every +1/-1 of rating, adjustment of $ 0.25 million is made.

iv. Cost to duplicate

The rationale behind this form of valuation is that typically investors would not want to invest more than what it would take to duplicate the business. This start-up valuation method requires a comprehensive evaluation of the assets of the startup to help determine the fair market value. This is one of the few approaches that does not necessarily look at the future of the start-up and also rarely used by investors.

v. Market multiple / Comparable transactions method

When using the market multiples approach, the potential investors could consider either the current market price of publicly traded peer companies or the previous comparable transactions with disclosed multiples. In start-up valuation, the most often used multiples are the following: enterprise value-to revenue (EV/R), enterprise value-to-EBITDA (EV/EBITDA), enterprise value-to-EBIT (EV/EBIT), and enterprise value-to-free cash flows (EV/FCF).

vi. Venture Capital method

As the name suggests, this method is a go-to for venture capital firms, and it's another option to consider if you need a pre-revenue valuation. It also reflects the mindset of investors who are looking to exit a business within several years.

There are two formulas you’ll use to work toward your valuation:

Anticipated Return on Investment (ROI) = Terminal Value ÷ Post-Money Valuation

Post-Money Valuation = Terminal Value ÷ Anticipated ROI

The exit value itself is derived from the famous multiple valuation methodology that investors use to assess the valuation of mature companies. Yet, whilst mature businesses often use EBITDA multiples, because start-ups often are unprofitable, and hence revenue multiples are generally used instead.

The venture capital valuation method is quite powerful as it solves an important problem: unlike other methodologies the VC method takes into consideration business, market and investor-specific factors.

vii. Discounted Cash Flow (‘DCF’) method

This method of startup valuation relies on a future-based approach. It makes predictions relating to the company’s future growth and potential profit. This method is the most suited for recently launched start-ups and paints a clear picture of the future. Discounted Cash Flow method helps decipher an accurate investment return rate and therefore helps forecast the business’s potential. It further highlights the scope of growth, making it a precise start-up valuation method.

DCF uses the future free cash flows of the company discounted by the firm’s weighted average cost of capital (the average cost of all the capital used in the business, including debt and equity), plus a risk factor measured by beta, to arrive at the present value.

The DCF method is a strong valuation tool, as it concentrates on cash generation potential of a business.