DECODING RULE 11UA INCOME TAX RULES, 1962

PRACTICAL HURDLES AND INTERPRETATIVE PERSPECTIVES

6/1/202513 min read

This article examines key interpretational and practical challenges in applying Rule 11UA and proposes possible views along with their underlying assumptions to support more effective and consistent implementation

Context and purpose of this article

This article critically examines the limitations in applying Rule 11UA for valuing unquoted equity shares. It highlights the practical complexities and inconsistencies arising from the prescribed valuation formula and explores interpretative methodologies that align legal compliance with underlying economic realities striving for adherence to the statutory framework while enabling a more accurate and meaningful valuation approach.

Governing provision

Section 56(2)(x)(c) states that Income shall be chargeable to income-tax under the head IFOS where any person receives from any person(s) on or after April 1, 2017 any property other than immovable property,

(A) without consideration, the aggregate fair market value of which exceeds fifty thousand rupees, the whole of the aggregate fair market value of such property;

(B) for a consideration which is less than the aggregate fair market value of the property by an amount exceeding fifty thousand rupees, the aggregate fair market value of such property as exceeds such consideration.

Further, Rule 11UA(1)(c)(b) provides methodology to determine FMV of valuation of unquoted equity shares.

The fair market value of unquoted equity shares shall be the value, on the valuation date, of such unquoted equity shares as determined in the following manner, namely: the fair market value of unquoted equity shares = (A + B + C + D - L) × (PV)/(PE),

Where,

A = book value of all the assets (other than jewellery, artistic work, shares, securities and immovable property) in the balance sheet as reduced by,—

(i) any amount of income-tax paid, if any, less the amount of income-tax refund claimed, if any; and

(ii) any amount shown as asset including the unamortised amount of deferred expenditure which does not represent the value of any asset;

B = the price which the jewellery and artistic work would fetch if sold in the open market on the basis of the valuation report obtained from a registered valuer;

C = fair market value of shares and securities as determined in the manner provided in this rule;

D = the value adopted or assessed or assessable by any authority of the Government for the purpose of payment of stamp duty in respect of the immovable property;

L = book value of liabilities shown in the balance sheet, but not including the following amounts, namely:

i. the paid-up capital in respect of equity shares;

ii. the amount set apart for payment of dividends on preference shares and equity shares where such dividends have not been declared before the date of transfer at a general body meeting of the company;

iii. reserves and surplus, by whatever name called, even if the resulting figure is negative, other than those set apart towards depreciation;

iv. any amount representing provision for taxation, other than amount of income-tax paid, if any, less the amount of income-tax claimed as refund, if any, to the extent of the excess over the tax payable with reference to the book profits in accordance with the law applicable thereto;

v. any amount representing provisions made for meeting liabilities, other than ascertained liabilities;

vi. any amount representing contingent liabilities other than arrears of dividends payable in respect of cumulative preference shares;

PV = the paid-up value of such equity shares;

PE = total amount of paid-up equity share capital as shown in the balance sheet;

Further, Rule 11UA(1)(c)(c) provides methodology to determine FMV of unquoted shares and securities other than equity shares in a company which are not listed in any recognized stock exchange shall be estimated to be price it would fetch if sold in the open market on the valuation date.

Interpretational Variances Arising from Adjustments Under Rule 11UA

1. Does an adjustment for Guideline value is required for ROU asset recognized as per Ind AS 116, Leases

A ROU asset, as per Ind AS 116, represents the lessee’s right to use an underlying asset (such as land or building) for a specified lease term. The ROU asset is initially measured at the present value of future lease payments and is recognized on the balance sheet along with a corresponding lease liability. The asset is subsequently depreciated over the lease term or the useful life of the asset, whichever is shorter.

Now the question arises here is whether such ROU asset be considered as immovable property and whether any adjustment for guideline value (i.e., assessed or assessable by any authority of the Government for the purpose of payment of stamp duty in respect of the immovable property) should be carried out as per Rule 11UA.

Possible views:

i) A ROU asset, as recognized in accordance with Ind AS 116 – Leases, merely represents the lessee’s right to use an underlying asset (such as land or building) for a specified lease term. Crucially, it does not equate to ownership of the asset, nor does it confer discretionary rights to sell, transfer, or dispose of the underlying property. It is akin more to an intangible right than an ownership stake in an immovable property. Accordingly, it should be treated same as intangible asset, to be reflected at its book value in FMV computations under Rule 11UA.

ii) Alternatively, the ROU Asset can be considered at the guideline value of the underlying asset, aligning with the principles of conservatism and the concept of substance over form. This perspective becomes particularly relevant in the case of long-term leasehold lands such as 99 years leases granted by Government agencies which in practical terms, function similarly to freehold ownership. In many cases, such leasehold land is allotted by central or state governments for specific purposes such as infrastructure development, industrial parks, set of specific industries etc. Although these leases are technically not freehold, the rights conferred upon the lessee are extensive: including rights to construct, use and even transfer the leasehold interest in some cases. These rights span the entire economic life of the asset, leaving only limited administrative restrictions. Hence such long-term leasehold arrangements may be viewed as equivalent to ownership of immovable property. In such cases, continuing to reflect the asset at its historical cost, particularly if allotted decades ago at nominal or concessional rates may not reflect its actual economic value.

2. When FMV of further investment in unquoted equity shares determined under this Rule is Negative

This issue may particularly arise when investments in unquoted equity shares are recorded at cost in the Company's books. However, the fair market value of such investments, as calculated under Rule 11UA, can often be negative, especially for early-stage or loss-making startups still striving to establish their market presence.

Possible views:

i) If the Company is legally obligated to fund the Investee Entity in case of its negative net worth, the investment should be considered at a negative value. This will be the case when investment in unquoted equity shares of subsidiaries is held.

ii) However, if no such liability exists, the investment should be considered at nil value owing to the reason that investment is in fully paid up equity shares and no further liability exists to the holders. Moreover, from conservative basis also, this view can be considered.

3. Multi-tier investments

We often come across scenario where the Company (FMV of whose equity shares is to be determined) further holds investments in shares and securities of other companies which in turn further hold investments and so on. This is typically referred as Multi-tier or Layered investment structure. Now the question here comes is till what level the further investments will be evaluated in determining the FMV of equity shares of the main Company.

Possible view:

The determination of fair market value should be based on materiality and judgment. Typically, valuation can be considered up to two layers of investment. For instance, if FMV needs to be determined for Co A, and Co A holds an investment in Co B, which in turn holds an investment in Co C, with Co C further holding investment in Co D, then separate FMV calculations will be required for Companies A, B, and C, reflecting valuation up to two layers of investment. When assessing the FMV of Co C, Co D may also be considered if its valuation is highly material in relation to Co A.

4. Scenario where the FMV of unquoted securities other than equity shares is to be determined

This is a scenario where FMV is to be determined pursuant to transfer of unquoted shares and securities other than equity shares. As per Rule 11UA(1)(c)(c), the FMV in such case will be the price it would fetch if sold in the open market on the valuation date. Now the Company whose FMV is to be determined say further holds investment in equity shares of other companies.

Let’s understand with example:

CCDs of Co. A are being transferred and hence FMV as per the above stated rule is to be determined using generally international valuation principles and standards. Further, Co. A holds investment in equity shares of Co. B. Question arises whether investment in equity shares of Co. B held by Co. A will be valued using the method prescribed under Rule 11UA(1)(c)(b) or 11UA(1)(c)(c)?

Possible views:

i) Primary purpose here is to value FMV of CCDs which will be as per applicable and relevant valuation principles and methods and accordingly valuation of equity shares of Co. B is just incidental and accordingly should be valued using same principles rather than Rule 11UA(1)(c)(b), as the primary objective here is to determine the value of the convertible instrument of Co. A, and there is no direct linkage to formula as per 11UA in this context.

ii) Alternatively, it could be argued that the nature of the securities involved necessitates a bifurcated approach, where CCDs are valued based on established valuation practices, while the equity shares of Co. B held by Co. A are separately valued using the prescribed formula under Rule 11UA for unlisted equity shares. This view emphasizes strict adherence to the rule’s textual interpretation, potentially leading to differing valuation outcomes depending on the adopted approach.

First view presented here is more practical and appropriate owing to the fact that Co. A’s value may also be significantly driven by value of Co. B. In that case following method prescribed under 11UA for Co. B might provide absurd result. More so, when Co. B is also a significant operating entity and Co. A’s overall value consists of value of holding in Co. B.

5. Treatment of taxes receivable (advance tax and TDS receivable) and provision for tax

The Rule says that any amount of income-tax paid, if any, less the amount of income-tax refund claimed, if any shall be excluded from the A portion of the formula prescribed in 11UA. Further, it also states that any amount representing provision for taxation, other than amount of income-tax paid, if any, less the amount of income-tax claimed as refund, if any, to the extent of the excess over the tax payable with reference to the book profits in accordance with the law applicable thereto should also be reduced from the L portion in the formula.

There were many ambiguities in the interpretation of these provisions which largely can be described as under:

· What tantamount to tax payable on book profits.

· Whether taxes paid considered above should be excluded while considering tax payable on book profits.

· Sch III requires advance tax and PFT for FY wise to be presented net in the Balance sheet. However, in notes, gross amounts can be disclosed.

· How refund claimed amount will be determined and adjusted.

Clarity in this matter have been finally made in Supreme Court’s judgement in the matter of Bharat Hari Singhania and Ors. Etc. Etc vs Commissioner of Wealth Tax. Even Schedule III of Companies Act, 2013 also states that provision for tax and advance tax should be presented as net and then gross amounts can be disclosed in notes. The objective of provision is to adjust any excessive provision from liabilities while computing FMV as per this Rule.

Possible views:

i) Both taxes paid and provision for tax are two sides of the same coin. These cannot be interpreted on individual basis. Since taxes paid is presented as net of provision for tax FY wise, in one view, no further adjustment is required assuming that there are no excess tax provisions and advance tax presented in FY are claimed / to be claimed as Refunds. As per this view, no adjustment either from asset / liability is required.

ii) Other view can be where taxes paid unless received are not considered as refund claimed and accordingly, total taxes paid need to be reduced in portion A of rule 11UA. This will though reduce FMV from IT perspective.

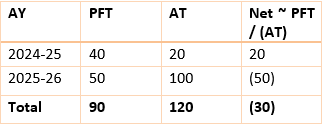

This can be better understood with example

Now here in FS as per Sch – III, this will be presented as below

Assets – Advance tax (Net) - (50)

Liabilities – PFT (Net) - 20

Following will be the number adjustments under above two views –

i) No adjustment required.

ii) Reduce 50 from A.

6. Treatment of the ESOP reserve part of other equity

The ESOP reserve represents the cumulative cost recognized in the books as per the applicable accounting standards — Ind AS 102 or AS 15 (as applicable) relating to share-based payments. This cost corresponds to the fair value of employee stock options (ESOPs) granted to employees and is recognized over the vesting period based on the number of options expected to vest. The reserve reflects a non-cash compensation expense and is presented under “Other Equity” / “Reserves and Surplus” (as applicable) in the Balance Sheet.

Possible views:

i) ESOP reserve represents an amount earmarked specifically for employees (against options granted), and not available to existing shareholders, it can be interpreted as an obligation / liability and reduced from balance of other equity or reserves and surplus (as applicable) and adjusted amount should be reduced from L. However, under Ind AS 102 (or AS 15), share-based payments are not considered liabilities unless the settlement is in cash. For equity-settled ESOPs, the standard treats them as equity transactions. This view is inconsistent with the accounting standards unless the ESOPs are cash-settled, in which case a liability classification is appropriate. Moreover, this will reduce the FMV.

ii) Alternatively, it should be recognized as part of other equity or reserve and surplus (not a liability) because it's a non-cash charge that will eventually convert to equity share capital when options are exercised. The reserve reflects the fair value of options granted, and upon exercise, it is transferred from ESOP Reserve to Share Capital and Securities Premium. While this view aligns with accounting principles, it may increase FMV per share subject to the increase in paid-up capital (PE) of formula prescribed under 11UA due to the consideration of issuance of new shares upon exercise of ESOPs which can lead to a dilution. This dilution, while increasing the PE in the formula, will decrease the FMV per share.

7. Treatment of equity and liability component of compound financial instruments

Ind AS 32, Financial Instruments, requires entities to separate the liability and equity components of convertible instruments like CCDs on initial recognition. Assuming CCDs with mandatory coupon are issued for say 5 years and convertible into fixed number of shares at the end of their term are in nature of compound financial instruments. The liability component of CCDs is computed by discounting the interest cash outflows for 5 years at an applicable incremental borrowing rate for a comparable loan. The equity component would be measured at the residual amount, after deducting the fair value of the financial liability component from the fair value of the entire compound instrument.

For example, Co. A has issued 100 million in CCDs, of which, based on Ind AS accounting principles, 70 million has been recorded as a financial liability and 30 million has been recorded as equity.

Now what should be the treatment of the 30 million recorded in other equity and 70 million recorded in financial liability:

Possible views:

i) In one view, since the purpose is to carry out the FMV of equity shares, total balance of CCDs (including equity component) should be considered as liability. This view is similar to treatment of ESOP reserve as explained above. However, this may distort the FMV especially in case where majority of funding happens in the form of convertible instruments (CCPS, CCDs) which are substantially akin to equity shares. With this view, the entire net worth will be attributed to equity shareholders which may not be commercially true when same computed on fully dilutive basis.

ii) Alternatively, the equity component can be included within reserves and surplus, while simultaneously increasing the number of outstanding equity shares to reflect the probable future conversion of CCDs attributable to the current equity portion.

8. When the Capital structure consists of CCPS as well

CCPS are hybrid financial instruments and have increasingly become a preferred mode of investment in the current market environment. While CCPS exhibit characteristics similar to equity shares, they offer preferential rights in terms of dividends and liquidation, distinguishing them from ordinary equity instruments. A key challenge arises in determining the fair market value of equity shares under Rule 11UA, particularly with respect to how CCPS should be treated in the capital structure during such valuation.

Possible views:

i) One view, though conceptually straightforward but often impractical, is to classify CCPS as liabilities when computing the fair market value (FMV) of equity shares. However, this approach may not accurately reflect the true economic substance of the instrument. Furthermore, such classification could result in a disproportionately higher FMV for equity shares compared to a valuation method that considers equity on a fully diluted basis.

ii) An alternative and more nuanced view considers the presentation of CCPS under Ind AS, where they are often classified as "equity instruments entirely in nature," especially when they involve fixed-to-fixed conversion terms and do not carry any obligation for mandatory dividends or interest payments. From this standpoint, treating CCPS as liabilities may be inappropriate. which aligns with the economic substance of CCPS as quasi-equity instruments, appears more appropriate and reflective of market realities. Again here also, conversion ratio if different from 1:1, will need to be appropriately adjusted for.

9. How should share application money pending allotment be classified under Rule 11UA?

In our view, since share application money has been received but no allotment has taken place, the amount should be classified as a liability as no shares have been issued as of the valuation date.

10. Treatment of investment in share warrants of listed entity

Sometimes company invest in share warrants of a listed entity as per SEBI -ICDR regulations applicable. In such scenarios, an initial investment to the extent of 25% of share price is made and balance is paid on exercise which is within 18 months. How this need to be treated under this Rule.

Possible views:

i) In one view, this can be revalued considering quoted price of the share on the date of valuation and considering in proportion to initial money paid against these warrants.

ii) Another view, could be since warrants give holders an option to convert these into shares at future date at the exercise price as determined now, this can be valued using the value it will fetch in open market since these are considered as other than equity shares and accordingly, an option pricing model can be used for its analysis. However, pls note that this is very complex and judgement should be applied considering the materiality.

11. Adjustment related to DTA / DTL

DTA and DTL represent timing differences that result in future tax benefits (reduced tax outflows) and future tax obligations (increased tax outflows), respectively. These are recognized on a net basis as either assets or liabilities in accordance with the relevant accounting standards and principles.

Possible views:

i) One view is that a DTA is a notional or non-cash asset and therefore should be excluded from the computation of assets under Rule 11UA. Similarly, any DTL should also be excluded on the same grounds.

ii) An alternative perspective suggests that DTA / DTL, being audited carried-forward balances with a reasonable certainty of future reversal, are akin to other ascertained liabilities or provisions. Therefore, they should be considered legitimate components of the balance sheet and not be adjusted or excluded in the computation of FMV under Rule 11UA.

Conclusion

The primary objective of Rule 11UA is to prevent tax abuse and avoidance, not to penalize genuine transactions that reflect economic substance. This article examines possible interpretations of the rule, with a focus on minimizing valuation distortions in practical scenarios. While not exhaustive, the perspectives shared aim to provide balanced guidance until the law evolves further taking into account developments such as Ind AS framework, modern capital structures owing to investments by private equity and venture capital firms.